What is the difference between Blockchain and Bitcoin?

Nowadays, cryptocurrency is making headlines worldwide, and many ordinary people seem to have made significant profits from trading in Bitcoin. However, for many, cryptocurrencies are a new concept, and people are keen to understand what is the difference between Bitcoin and Blockchain.

In this article, we’ll differentiate between blockchain and Bitcoin and their use in cryptocurrencies. Before going into differences, it’s essential to understand both of these terms.

On this page:

What is Blockchain?

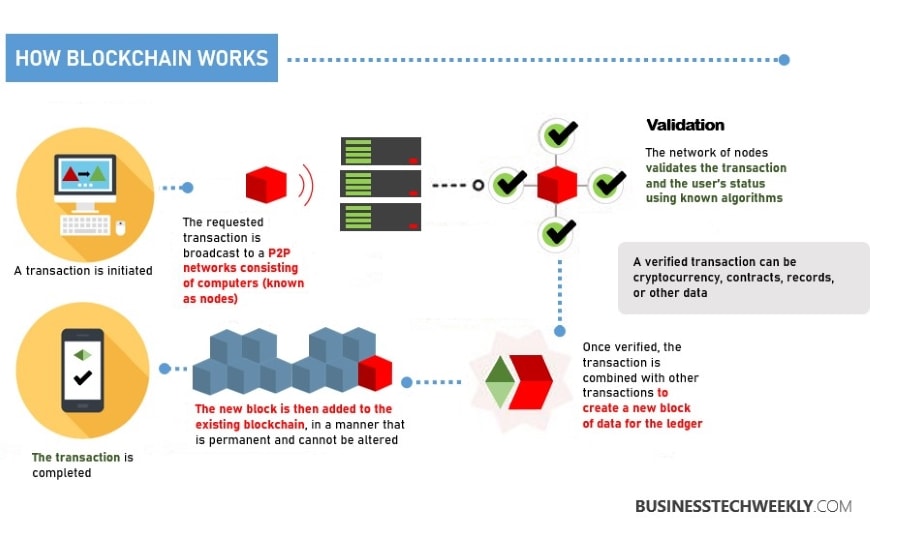

It is a digital payment gateway that regularly and correctly records transactions between two parties. Blockchain is a technology restricted to digital assets, particularly Bitcoin. It allows parties to share valuable data, transact, and securely pool their digital resources.

Many people assume that it’s the latest technology; however, it’s not the case. It came into existence in 1991, but it got famous after the advent of cryptocurrencies. Blockchain may be challenging to regulate and understand. It’s a decentralized technology made of three concepts such as blocks, miners, and nodes.

- Blocks – In the blockchain, each chain consists of blocks, and they contain all the information about the transaction. Moreover, each block has a unique hash and nonce stored linearly and chronologically at the end of the blockchain. When the chain increases, it becomes difficult to go back and make changes in the chain.

- Miners – They help to create multiple blocks. Considering the composition of the neighborhood, it is a complicated task.

- Nodes – The third important concept is the understanding of decentralization within the blockchain. Nodes help to maintain integrity and privacy of privacy. Moreover, they prevent data breaches through systematic or unsystematic information exchange.

Related: Blockchain Principles: Understanding Blockchain Technology

What is Bitcoin?

It is the earliest cryptocurrency that has used blockchain technology to facilitate peer to peer payments. It uses a decentralized network and offers a low transaction fee than other popular payment gateways.

To trade Bitcoin, you first need to get a Bitcoin wallet and software to receive, send, and store funds.

You can download the software on a PC, mobile phone, or any other digitally supported device. The second step is to earn Bitcoin, and you can do this through trading, requesting payments from a client, and playing online games.

See Also: What is a Bitcoin Wallet and How does it work?

Bitcoin is a different currency from other currencies because a central banking system does not govern it. Moreover, they’re stored physically. A mathematical algorithm is used to secure a string of numbers stored in a private and public key. You can consider a public key as the bank account number, and the private key is the ATM pin.

Bitcoin sounds complex, but it’s an easy currency to understand. Anyone can send and receive Bitcoin. You can quickly pay and get paid. To send and receive Bitcoin, you’ll have to create a wallet and put the address into any digital currency platform.

Differences between Blockchain and Bitcoin

For someone new to either blockchain or Bitcoin, it’s pretty normal to use the terms interchangeably. However, they are different. Let’s explore some most significant differences between the two terms:

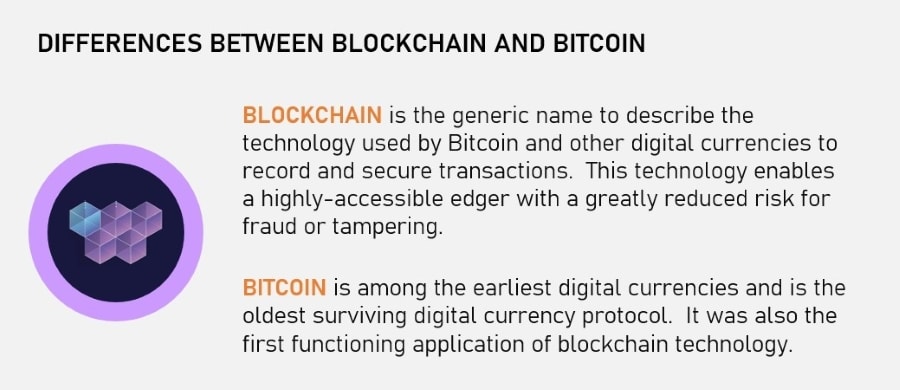

- Blockchain is a technology, and Bitcoin uses blockchain for anonymous and secure transactions.

- Bitcoin operates on anonymity, and blockchain is a transparent mechanism.

- Blockchain has been used extensively, but Bitcoin is only restricted to digital currency exchange.

- Blockchain transfers digital assets, proprietary information, rights, etc. Bitcoin can only transfer digital currencies.

People need to understand the relation between blockchain and Bitcoin, especially those who use online payment gateways to send, receive, and store currency. However, blockchain technology has many other uses as well, along with regulating Bitcoin.

Furthermore, blockchain can automatically help release agreed payments and execute smart contracts. It allows you to maintain a transparent system of audit supply chains, record and provide proof of insurance.

What is the future of Blockchain and Bitcoin?

Blockchain technology is dominating our internet spaces. You need to be cautious when dealing with cryptocurrencies. For example, when you pursue crypto gambling, ensure that you use trustworthy service providers. Websites often use third-party service providers for converting Bitcoin deposits into digital currency.

Blockchain and Bitcoin both remain mostly unregulated throughout the world because of their complex structures. So, you have to be cautious when using Bitcoin for transactions. However, the commonly held view is that both Bitcoin and blockchain will dominate the digital world in the future.

Key Distinctions between Blockchain and Bitcoin

Both online and offline businesses are adopting blockchain technology and accepting Bitcoin payments worldwide. Sooner or later, this technology will take over the traditional payment gateways like PayPal and Visa. Moreover, it will change the way of processing payments and makes them more accessible and safer options.

- Blockchain is a distributed database, whereas Bitcoin is a cryptocurrency.

- Bitcoin is using blockchain technology, and blockchain has many other users.

- Blockchain is about transparency, while Bitcoin promotes anonymity.

- Blockchain can be used to transfer several types of information, such as ownership rights, contracts, and property. On the other hand, Bitcoin only moves currency between the users.

Why is Blockchain Important?

A significant advantage of blockchain’s distributed ledger is the reduced operational costs. Blockchain removes the need for intermediaries, thereby eliminating the administrative effort of record keeping and transaction reconciliation and consequently removing fees from existing processes.

Furthermore, by removing the data gatekeeper (middleman), blockchain enables businesses to quickly and easily trace products and transactions back to their roots. This ability results in time savings, which also lead to considerable costs savings.

This efficiency provides authenticity, reliability, and transparency, as well as security. Since data is shared — and validated before it’s recorded — in multiple countries on multiple systems, it is more secure.

Businesses and organizations have become aware of these benefits and the advantages of embracing blockchain technology offers. From healthcare to the supply chain and beyond, blockchain has wide-reaching possibilities.

For example, regulated organizations, such as finance, insurance, and healthcare, registering and filing state-mandatory documentation, or states using the technology for electronic absentee voting.

From these examples, it’s clear blockchain will be crucial in smart cities.